Quantitative insights on how the COVID-19 pandemic has impacted e-commerce for retail in the United States. Statistics on how e-commerce behaviors have changed between pre-COVID times and today have also been provided. A brief description of each impact and the relevant quantitative data points have been provided as well.

- The COVID-19 pandemic has prompted considerable restrictions on physical encounters. Self-imposed social isolation to avoid catching the disease, along with stringent confinement measures, has effectively halted a big portion of old-fashioned brick-and-mortar retail in the short term.

- Between February and April 2020, retail and foodservice revenue in the United States decreased by 7.7% compared to the same period in 2019. However, sales climbed by 16% and 14.8% respectively, for food stores and non-store retailers, mostly for e-commerce stores.

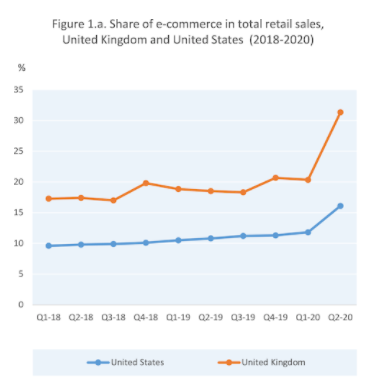

- While the share of e-commerce in total retail in the United States progressively increased during the first quarters of 2018 and 2020 (from 9.6 percent to 11.8 percent), it jumped to 16.1 percent in the first and second quarters of 2020.

- The pandemic also drove many Americans to shop online, resulting in an additional $105 billion in e-commerce revenue in 2020, and speeding up the transition to e-commerce by two years.

- According to the report from the Commerce Department, online sales reached $791.70 billion in 2020, increasing 32.4 percent from $598.02 billion in 2019. That is the highest annual growth rate recorded for online sales in any year for which data are available.

- Due to store shutdowns and buyers’ fear of getting the coronavirus in public, e-commerce blossomed in 2020. Additionally, data from Q1 2021 indicate that the coronavirus continues to have an effect on retail expenditure. In Q1 2021, online sales rose 39 percent year over year, nearly tripling the 14 percent growth in Q1 2020, and outpacing both Q3 and Q4 2020 figures.

- The rapid growth in e-commerce in 2021 is likely due to customers spending their stimulus checks and tax refunds. Furthermore, with coronavirus cases surging in January, many consumers continued to avoid stores in favor of online shopping. This situation, combined with buyers starting to buy items for their post-vaccine journeys such as luggage, teeth whitener, and vacation attire, all became a factor to the 39% surge.

- The COVID-19 crisis’ impact on e-commerce is not consistent in all product categories or vendors. In the United States, demand increased for essential products such as personal protection items (e.g. disposable gloves), home activities supplies, groceries, and ICT devices

- However, demand has decreased for travel and sports-related items, as well as formal wear. Some of these products include suitcases, bridal clothing, gym bags, and others.

- Based on the data of 200,000 third-party Amazon suppliers in the United States, approximately 36% of vendors were not actively selling in April 2020, up from roughly 28% in February.

- Vendors with fewer than 1,500 product listings (ASINs) were particularly impacted, whereas sellers with more than 3,000 listings witnessed an increase in sales. These figures demonstrate how the COVID-19 pandemic may have resulted in a demand transition away from smaller, more specialized vendors, and toward bigger and more diversified merchants.

- Additionally, the COVID-19 scenario accentuated the complementarity of online and offline sales channels.

- This complementarity was seen when Amazon’s own sales increased by 26% in the first quarter of 2020 but its cut in the overall e-commerce in the United States decreased from 42.1% in January 2020 to 38.5% in June 2020.

- Amazon, in particular, lost a portion of its market to Walmart (from 4.2% to 5%) and Target (from 2.2% to 3.5%).

- It can then be deduced that these and similar businesses gained some advantage from extensive networks of brick-and-mortar locations, which enabled rapid delivery and pick-up (kerbside fulfilment).

- Around 21% of American adults mentioned that they have ordered groceries online or via an app from a local store as a direct response to the pandemic. The percentage stayed almost on the same level (19%) among only those aged 65 years and above.

- As convenience has always been a primary motivator for e-commerce channel usage, it is highly probable that most of the new converts will continue ordering at least some products from digital stores in the future. Others might keep ordering online due to a lingering fear of a pandemic repercussion or because sellers were able to keep them through new loyalty programs or subscription plans.

- On the supply side, many brick-and-mortar store owners who previously faced closure are now viewing e-commerce as a critical supplemental or alternative sales channel.

- Due to the investments that were already spent to transition to online sales, many enterprises that increased their e-commerce involvement during the pandemic have an incentive to leverage on their newly-added infrastructure or capabilities on a long-term basis.

- This is especially true for bigger retailers that have added investments in their internal sales and distribution systems.

- As an example, by April 12, 2020, Amazon’s supermarket subsidiary, Whole Foods Markets had expanded its online order capacity by more than 60% in response to the jump in demand, scaling pickup services from around 80 branches to over 150 locations. Additional expansions are highly probable in the future.

- Even smaller sellers, most of whom have avoided investing in online systems and just leveraged on the existing infrastructure and services from various digital platforms (e.g. “fulfillment, logistics, and customer support”), might opt to fully use their established online presence and experience into a “long-term asset.”

- A similar argument could be made for a variety of other firms, many of which are just now building the framework for an online sales system in reaction to regulatory easing. Some of these businesses include “cafes, restaurants, museums or public swimming pools,” which were compelled to implement online booking systems to manage the flow of people in their spaces at any given moment.

- Between January and mid-April 2020, the Federal Trade Commission (FTC) received over 22,000 consumer complaints over COVID-19 frauds, resulting in customer losses of over $22 million. Certain phishing, ransomware, and identity theft fraudulent cases have duped consumers into sharing their information by posing as health or disease control associations such as the World Health Organization. Other nefarious schemes attempt to deceive consumers financially, including phony charity scams and prominent corporate impostor frauds.

- In addition to these deceptive practices, some scammers have resorted to advertising hygienic items that never got delivered, or selling bogus COVID-19 test kits.

- Scammers have also spread false and scientifically unsubstantiated claims that some items that they sell can prevent or treat symptoms of COVID-19. As a result, the US Federal Trade Commission (FTC) issued warning letters to more than 60 companies (many in collaboration with the US Food and Drug Administration) regarding deceptive claims about homeopathic drugs, essential oils, traditional Chinese medicine, salt therapy, and vitamin immune boosters.

- Consumers have also suffered from price gouging, as some companies have attempted to maximize profits from heightened demand for necessary commodities such as face masks and hand sanitizers, as well as essential grocery items or printers, by drastically increasing their prices.

- Consumer trust is critical for markets to operate properly. This is especially true in e-commerce because buyers cannot actually verify the goods being sold remotely.

- As consumers migrate online and certain dealers are bent on abusing their weaknesses, many firms have become aware of the critical nature of trust-building. In March, a survey of US consumers revealed that 52% of respondents prefer to do business with organizations that publicly safeguard their customers and employees from COVID-19 dangers.

- As a response to the pandemic, several firms have altered their consumer policies. Some offered free shipping, others increased the time limit for change-of-mind returns, and some waived cancellation fees. Additionally, they are highlighting choices such as no-contact delivery or pick-up.

- Given their significant proportion of e-commerce business, online marketplaces are now actively checking their sites for scams, exorbitant pricing, and false health claims. They are also taking out fraudulent listings or suspending accounts as necessary. They are also advocating for stronger government assistance in identifying unscrupulous traders.

- Consumer protection authorities have acted swiftly to notify consumers of critical pandemic-related concerns, and several are considering unique steps. Confronted with the issue of taking into account both user health and safety protection with support for firms and employee protection, the authorities have given exemptions from consumer protection regulations when it is for the good of the public.

- For instance, several agencies have expedited the clearance procedure for new items such as hand sanitizers to facilitate the availability of these products to the consumers.

- In the United States, competition authorities have given recommendations on how firms can work together to safeguard the population’s health and safety in the face of the pandemic.

- Social commerce has been greatly boosted by the pandemic. The sector is positioned for more growth as major social commerce platforms have improved their shopping and checkout functionalities.

- The eMarketer report projected that the “US retail social commerce sales will grow by 34.8% to $36.09 billion in 2021, accounting for 4.3% of all retail online sales. The growth rate forecast for 2021 was also changed from 19.8% originally to 37.9%.

- Apparel and accessories continue to be the biggest best-sellers in the social commerce channel. Consumer electronics, cosmetics, home décor, and consumer goods are other significant categories.

- Meanwhile, the EY Future Consumer Index (Index) report revealed that 80% of American consumers are still transforming their shopping habits as the pandemic continues to spread.

- Around 60% are going to physical stores fewer times compared to pre-pandemic days. Around 43% purchase online more frequently for items that they used to purchase in brick-and-mortar stores.

- According to the report also, 38% of shoppers plan to do more shopping online and go to stores that can give them satisfactory experiences.

- The report also revealed that 37% of American consumers will shop online and pick up in-store more frequently in the future.

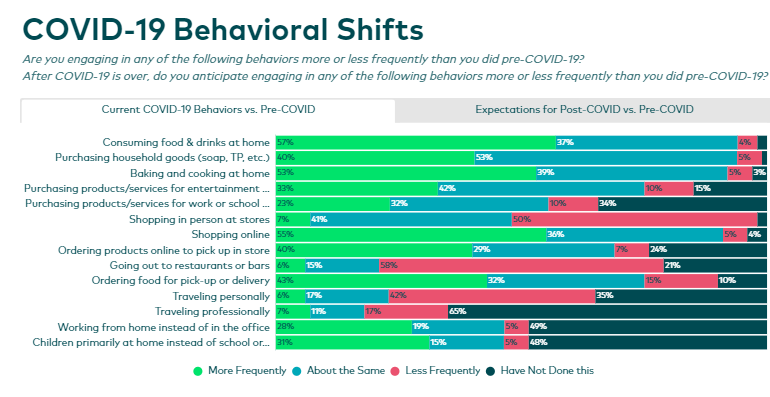

- At the moment, more than half of customers report baking, cooking, and enjoying food and beverages at home more frequently than they did prior to COVID. Around a quarter believe that these behaviors will persist once the pandemic is gone. Around 79 percent of consumers have reduced or eliminated their visits to pubs and restaurants during the pandemic, while 43 percent have increased their reliance on take-out or delivery. Following COVID, these behaviors’ intentions are divided: 32% intend to make up for lost time by visiting pubs and restaurants more regularly than they did prior to covid, while 23% anticipate continuing to go less frequently. 18% believe they will increase their frequency of ordering take-out and delivery, while 19% believe they would decrease their use of the service post-COVID.

- When it comes to purchasing, 55% make more online purchases during COVID than they did previously, while 50% make fewer in-store purchases. Following months of curtailed activity, 22% plan to retain a higher frequency of online buying, while 28% intend to increase their frequency of in-store purchasing.